The Dubai real estate market has entered 2026 with extraordinary strength but also with signs of structural evolution. After the historic peaks of 2024 and 2025, the market is transitioning from a pure growth cycle into a more mature, data-driven, and investor-focused phase.

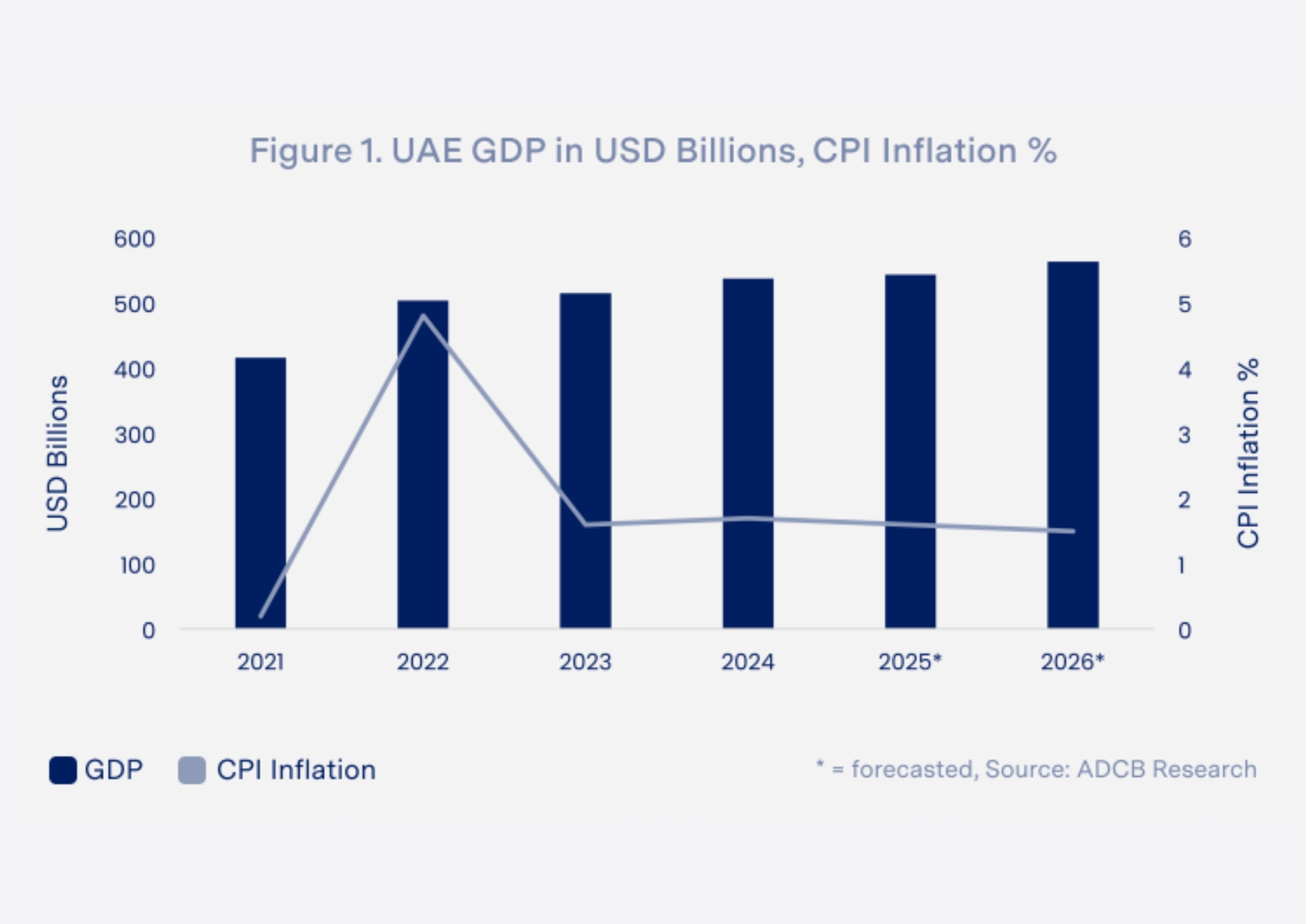

The UAE’s economy is the second largest in the GCC (Gulf Cooperation Council), with a robust track record of growth, particularly in its post-COVID recovery. GDP growth reached 3.8% in 2024, with forecasts projecting an increase to 4.2% in 2025 and 5% in 2026. This expansion has been driven by both oil and non-oil sectors, with the country’s diversification amplifying the role of non-oil industries such as trade, manufacturing, tourism, real estate, finance, and insurance in shaping GDP. For the emirate of Dubai, tourism and real estate remain key pillars. Meanwhile, CPI inflation has remained relatively low, reflecting the economy’s stability and strong purchasing power.

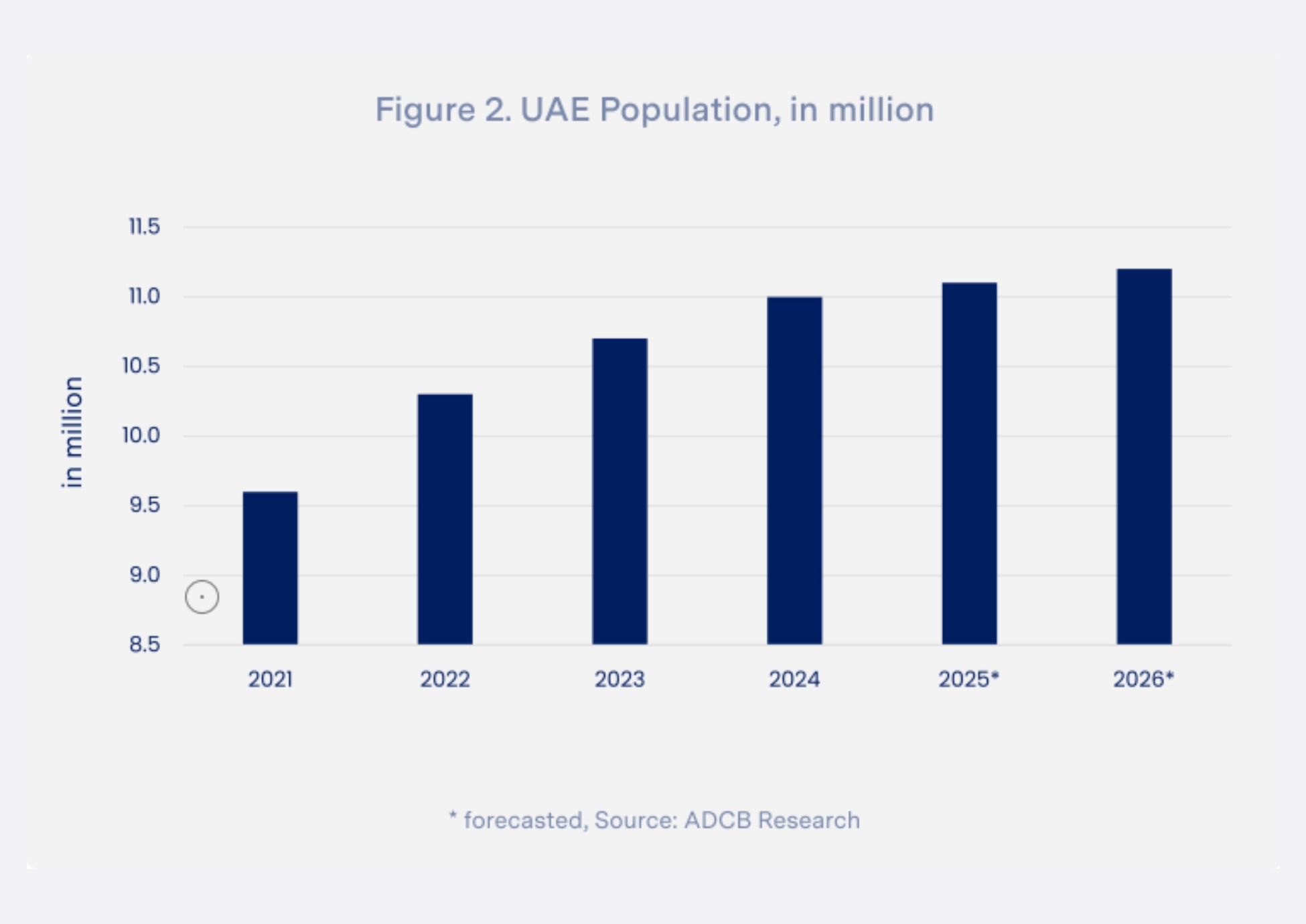

The UAE’s population continues to grow steadily,

fueled by its robust economy and business-friendly policies. Dubai and Abu Dhabi remain top destinations for expatriates, offering tax-free incomes and high living standards, while emirates like Ras Al Khaimah are gaining traction. Government initiatives such as the Golden Visa program have further boosted long-term residency.

Now housing one-third of the UAE’s population, Dubai has grown from 3.8 million to 4.1 million residents. Beyond employment opportunities, the emirate is emerging as an education hub, with private schools seeing 6% enrollment growth and universities

experiencing a 29% surge in international students. This combination of economic prospects, favorable policies, and educational development solidifies the UAE’s position as a premier global destination.

January 2026: A Historic AED 72.4 Billion Milestone

According to official figures from the Dubai Land Department (DLD), January 2026 marked the strongest opening month in the emirate’s history.

Property Sales: AED 72.4 Billion

Total Transactions: Exceeded AED 100 Billion (including mortgages/transfers)

Why This Matters:

This isn’t just a “big number.” It represents a major year-on-year increase compared to 2025 and confirms that global capital inflow remains aggressive across off-plan, secondary, and luxury segments.

The Evolution: 2024 – 2026

To understand where we are, we must look at how we got here:

2024 (The Foundation): The acceleration phase. Characterized by double-digit price appreciation and rising rental rates driven by rapid population growth.

2025 (The Expansion): The year of dominance. We saw record annual transaction values and aggressive investor demand, particularly in the luxury off-plan sector.

2026 (The Strategic Shift): Strength with selectivity. While the market remains powerful, it is becoming smarter.

The Key Change: We are seeing a transition from emotional buying to strategic investment.

Key Market Drivers in 2026

1. Supply Pipeline & Absorption

Supply is the primary variable this year. A substantial number of units are scheduled for delivery in emerging master communities and mid-market clusters.

High Absorption: Prices stabilize and grow moderately.

Oversupply (Local): Specific zones may see price pressure. Success in 2026 depends on micro-market selection.

2. Rental Market & Yield Perspective

Dubai remains a global leader for rental returns, with average gross yields between 6% and 8%.

Drivers: Corporate relocations, long-term visa programs (Golden Visa), and zero personal income tax.

3. Segment Dynamics

Luxury Segment: Ultra-prime waterfront villas remain “bulletproof” due to limited inventory.

Mid-Market: More sensitive to new supply; price growth is moderating.

Off-Plan: Buyers are now prioritizing developer reputation and realistic completion timelines over flashy marketing.

Comparative Analysis: 2024 – 2026

| Factor | 2024 | 2025 | 2026 |

| Market Phase | Acceleration | Expansion | Strategic Stabilization |

| Price Growth | Rapid | Strong | Moderating |

| Supply | Controlled | Increasing | High Pipeline |

| Investor Behavior | Confident | Aggressive | Selective |

| Rental Yields | Strong | Strong | Stable |

Risk Factors to Watch

A balanced outlook must acknowledge potential headwinds:

Increased supply in specific sub-communities.

Global economic shifts and interest rate fluctuations.

Overconcentration in speculative off-plan projects.

The Safety Net: Unlike previous cycles, the 2026 market is protected by stricter regulations, robust escrow laws, and a highly diversified buyer pool.

What Happens Next?

Short-Term (2026): High liquidity and strong transaction activity, but with increased buyer selectivity.

Mid-Term (2027 – 2028): A “supply absorption” phase leading to sustainable, long-term appreciation.

The Bottom Line: Dubai is evolving into a global wealth hub. The record AED 72.4 billion January performance is a signal that while the “easy money” phase has passed, the institutional investment phase has arrived.